Nvidia GPU Debt Backstop Unleashes the AI Project Trinity: Capital, Offtake and Datacenters

Over 7T AI debt by 2029, There can be no Neoclouds without the Trinity. Nvidia's Backstop Economics Explained. AI Debt Needs Quantified. Nvidia's Objective is to Broaden Compute Access

Up until now the majority of AI buildouts have been primarily cashflow funded by the hyperscalers such as Google, Amazon, Meta, Microsoft, Oracle. Over the last year, that's started to turn with Oracle then Meta, and now even Google turning to debt. Nvidia revenue is skyrocketing, and even 3 years into the build out, the general market is still materially lower on shipment volumes and revenue estimates for Nvidia in the 2nd half of this year versus our through supply chain tracking in the Accelerator Model.

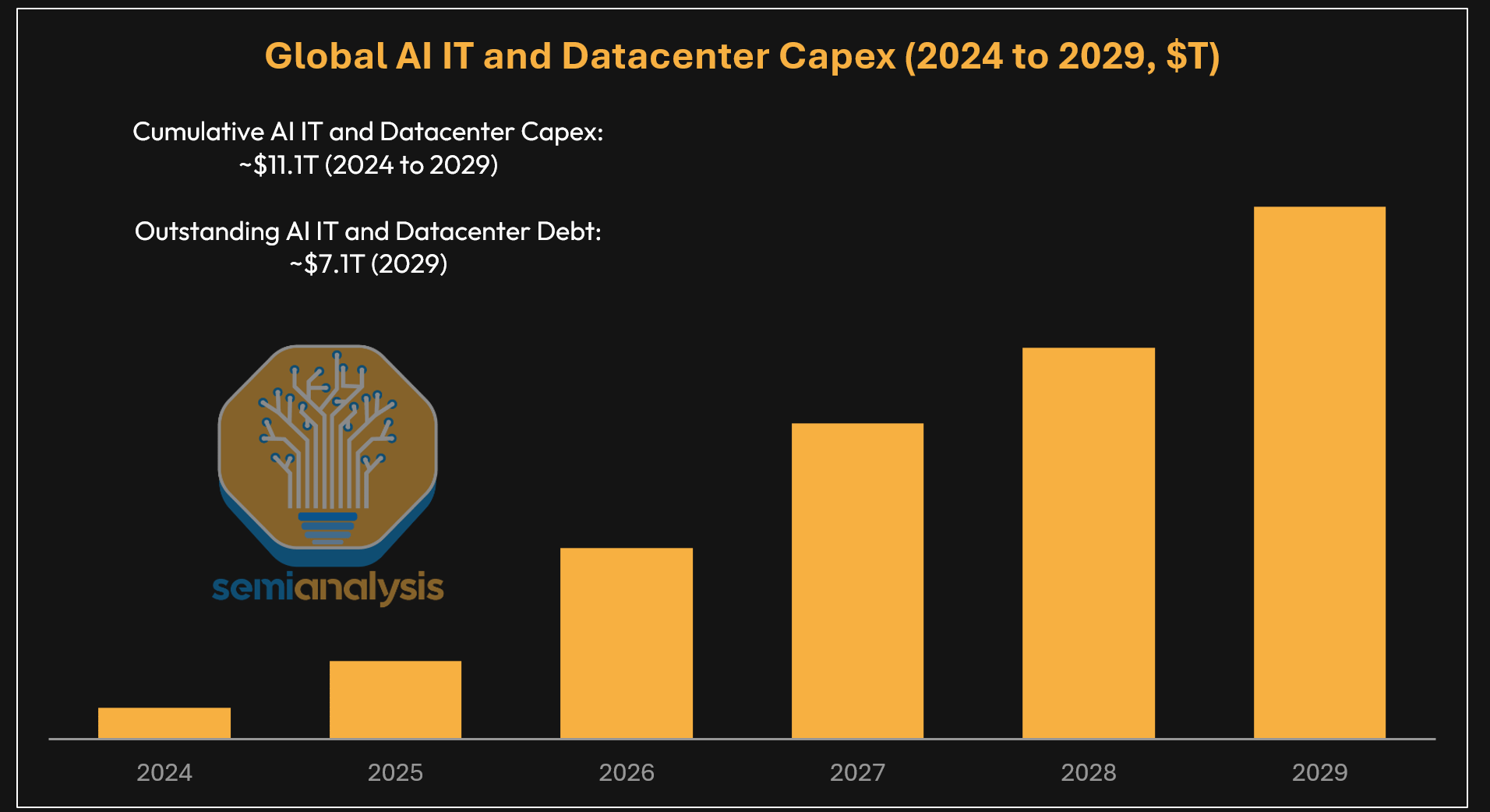

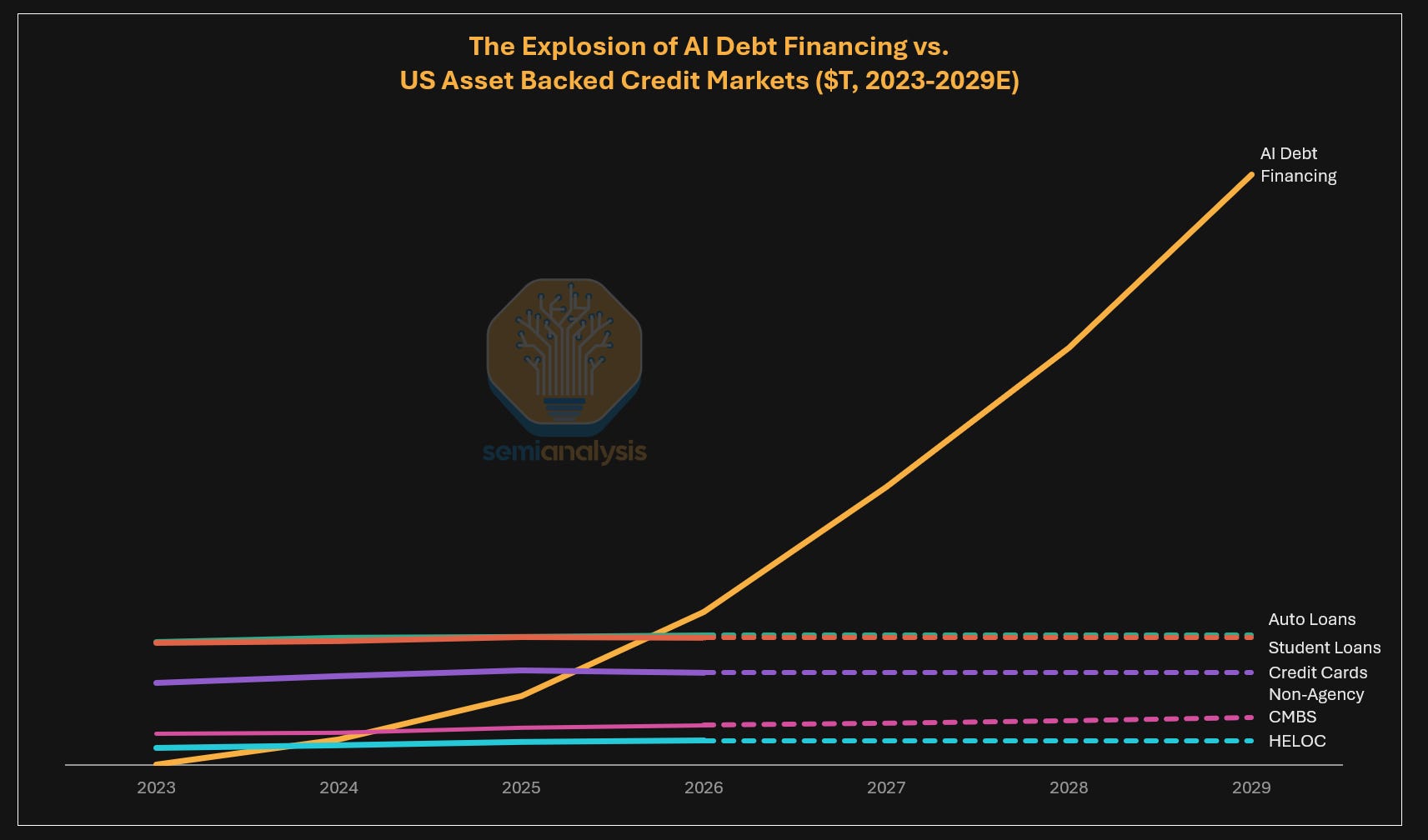

AI Debt Financing will become a multi-trillion-dollar credit market, with over $7T of debt outstanding by 2029 driven both by AI IT Capex and AI Datacenter Capex needs for Neoclouds, datacenter builders, and even hyperscalers. This will make it the second largest asset backed debt market after the US mortgage-backed financing market at just over $13T.

Annual AI Capex – including GPUs, networking, storage and attached CPU compute as well as for the Datacenters to house AI compute – will be well north of $2T in 2028. Cumulative AI Capex from 2024 to 2029 will reach ~$11.1T, and credit markets will be the main funding source for this buildout.

The surge in borrowing requirements to date has driven by briskly growing demand from AI labs and hyperscalers, and the construction of AI clusters to service this demand was made financeable by long-term take-or-pay compute contracts backed by hyperscalers, with the most common offtake period being 5 years. Though this article will mainly focus on financing AI IT Capex - that is, GPUs and related capex like storage, networking and CPUs attached - there is much that also needs to be done to support the growth of datacenter capex financing. A much more detailed breakdown of both AI IT Capex and AI Datacenter Capex can be found in our AI TCO Model and AI Datacenter Model respectively.

Executing on any AI Compute buildout requires assembling all three legs of what we call the AI Project Trinity – Capital, Offtake, Datacenter:

Capital: As of today, lenders require an offtake contract or a backstop from an investment grade hyperscaler before they will provide debt financing.

Offtake: To secure an offtake, you first need equity capital to demonstrate you can place deposits for the required IT equipment, but to raise equity – one needs to demonstrate that they have an offtaker and lenders in place!

Datacenter: Lastly, an aspiring Neocloud must either have a solid offtaker and lending lined up in order to convince datacenter operators to rent colocation to them, or the Neocloud must build a datacenter themselves.

Yet this is far from an impossible trinity, and many Neoclouds have been executing on cluster build-outs. Deals have been happening, but they come together thanks to clever structuring of one or more legs of the Trinity, close sponsorship of or matchmaking by capital providers like private equity firms that have been serial providers of capital to Neoclouds and Datacenters, and of course, some good old-fashioned risk taking on the part of everyone involved.

Our forecasts for GPU shipments and datacenter capex for the next few years imply that the total outstanding AI debt financing needs will quickly surpass the size of all other US asset backed markets.

But growing this debt market from hundreds of billions in 2024 and 2025 to ~$7.1T by 2029 is no mean feat – there are a number of significant obstacles that must be overcome for the debt market to reach this size and for the compute market to serve more than just hyperscalers and large AI labs:

Hyperscaler backstops are not infinite: Hyperscaler balance sheets will not be able to backstop trillions of dollars’ worth of compute, yet outside of the four corners of a 5-year hyperscale backstopped compute deal, the appetite to lend drops off almost entirely. If the lending market does not evolve beyond this template, once hyperscalers exhaust their capacity to backstop deals, there will be no further projects to lend to.

Lenders are still on the learning curve: Private credit and private equity have led the charge on lending to the first batch of large Neoclouds, but as spreads compress over time, and as capital needs increase, a broader set of lenders will need to be tapped, yet most banks still have a nascent understanding of AI Cluster total cost of ownership, the AI compute market as well as tokenomics and end demand and still hide behind the shield of an investment grade offtake or backstop.

Capital providers lack tools for pricing and managing risk: There are very few well-constructed price indices for GPU rental outside of our own SemiAnalysis GPU Rental Pricing Index. GPU rental transactions are all on a bilateral basis and not generally publicly available, and there is no active derivatives market to provide a pricing signal or a good reference for GPU residual value.

The current Neocloud market structure has a few other issues. The most pressing problem to solve is broad-based access to compute for renters other than hyperscalers and large AI labs, as well as the limited supply of shorter-term rentals given that most lending is for the 5y backstop template.

For example, VC-backed AI startups and inference providers may be cash rich, but they want large clusters on short term contracts so they can quickly get to their next round of funding and reload on compute. With most Neoclouds thus far preferring to stick with doing large 5y offtakes, these startups are forced to take on larger prepayment or longer contracts than they want, rent fewer GPUs than they need, end up using different GPUs than they would prefer, and often have to settle for start dates far into the future.

Inference providers in particular are very contracted time sensitive compared to training focused AI Labs. While AI Labs are able to commit for longer periods like 3 years and beyond, inference providers are completely unwilling to sign for longer than 1y and would rather forego access to compute than take the risk of committing for any extended period of time.

When it comes to shorter-dated rentals for everyone else, it is still a seller’s market. At this point, we are only aware of a few Neoclouds that are still offering 1y rentals, and they are setting aggressive terms for rental – sometimes requiring prepays of up to 100% of the total contract value. Neoclouds have so much demand for their GPUs that they are able to solve for a prepay amount that can entirely fund the cluster capex, meaning a theoretically infinite IRR as they can stand up a cluster with no cash out the door on their part!

Enter: The Nvidia Backstop

In 2025, we wrote extensively about how datacenter capacity was the bottleneck for AI compute growth. By early 2026, the datacenter supply situation improved considerably, but it became clear that chip production was now the limiting constraint. Now – mid-way through the year – it is clear that financing will now be one of the most significant obstacles to ramping large scale compute broadly available to everyone.

This is why Nvidia has stepped in and has started backstopping GPU rental offtakes themselves. In the backstop program, Nvidia provides a take-or-pay commitment to Neoclouds – a minimum revenue guarantee on the underlying GPU capacity. In exchange for this backstop, Nvidia also shares in a portion of the Neocloud’s revenue earned above the backstop level.

The Neocloud is of course free to rent to any other customer they would like for any term length they deem commercially reasonable and indeed the intent is for the Neocloud to never actually have to invoke the backstop.

Nvidia’s backstop program has a few key objectives:

To broaden compute availability: This objective has two dimensions, to open up the compute market well beyond just a few large hyperscalers and AI labs and to ensure rental contracts of varying contract terms (tenor) are available and not just 5y terms – particularly short terms of less than 1 year,

Support evolution of the GPU financing market: To ease lenders into funding Neoclouds with a varied book of clients and rental contract tenors by buying time for lenders to get up the learning curve and adopt tools to price and manage risk,

Grow Neoclouds: Provide early support so Neoclouds can grow rapidly and establish a track record and demonstrate the viability of their business model and client books so that they can become platforms that can be banked on attractive terms as well as take up datacenter obligations with greater ease. This broadens the base of buyers beyond just a few hyperscalers that will pit their own custom silicon solutions against Nvidia’s systems.

With this backstop in hand – the Neocloud can much more easily assemble the AI Project Trinity:

Capital: Lenders look to Nvidia’s backstop and its AA/Aa2 investment grade credit rating and are satisfied to lend matching the length of the backstop. With a viable go to market plan and an Nvidia backstop, equity can be raised to fund deposits to secure equipment and the various payments needed to start developing the cluster.

Offtake: Having the backstop in hand and with funding for the cluster, Neoclouds can then tap previously unaddressed offtake demand outside of just the typical 5-year AI lab or hyperscale offtake.

Datacenter: However, even with the backstop in place, securing the final leg of the Trinity and obtaining datacenter capacity remains challenging absent a creative datacenter rental structure or resorting to a self-built datacenter. Here, Nvidia is diving even deeper, as it has started backstopping datacenter leases.

The incremental revenue from the backstop program will be significant, but Nvidia stands to gain far more from these backstops than this additional revenue. They aim to do nothing less than entirely reshape the structure of the GPU market itself. We have already discussed how the TAM they can sell into will become bottlenecked very soon if a 5y hyperscaler backstopped offtake is the only viable deal structure.

In January 2026 for institutional subscribers, we first discussed how Nvidia was becoming the Central Bank of AI. A central bank exists to supply liquidity when others in the banking system are unwilling to step in, supporting economic activity until others are ready to take over.

Most in the neocloud ecosystem are unable to raise enough debt for large GPU buildouts unless they lease to the big hyperscalers directly. Nvidia doesn't want the market to be the same handful of concentrated buyers. The small buyers want GPUs, can pay for them, but they can't offer credit ratings to creditors funding the build out. In mid-2026, Nvidia is clearly showing it stands ready to offer this support as the central bank.

How Nvidia’s Backstops are Structured

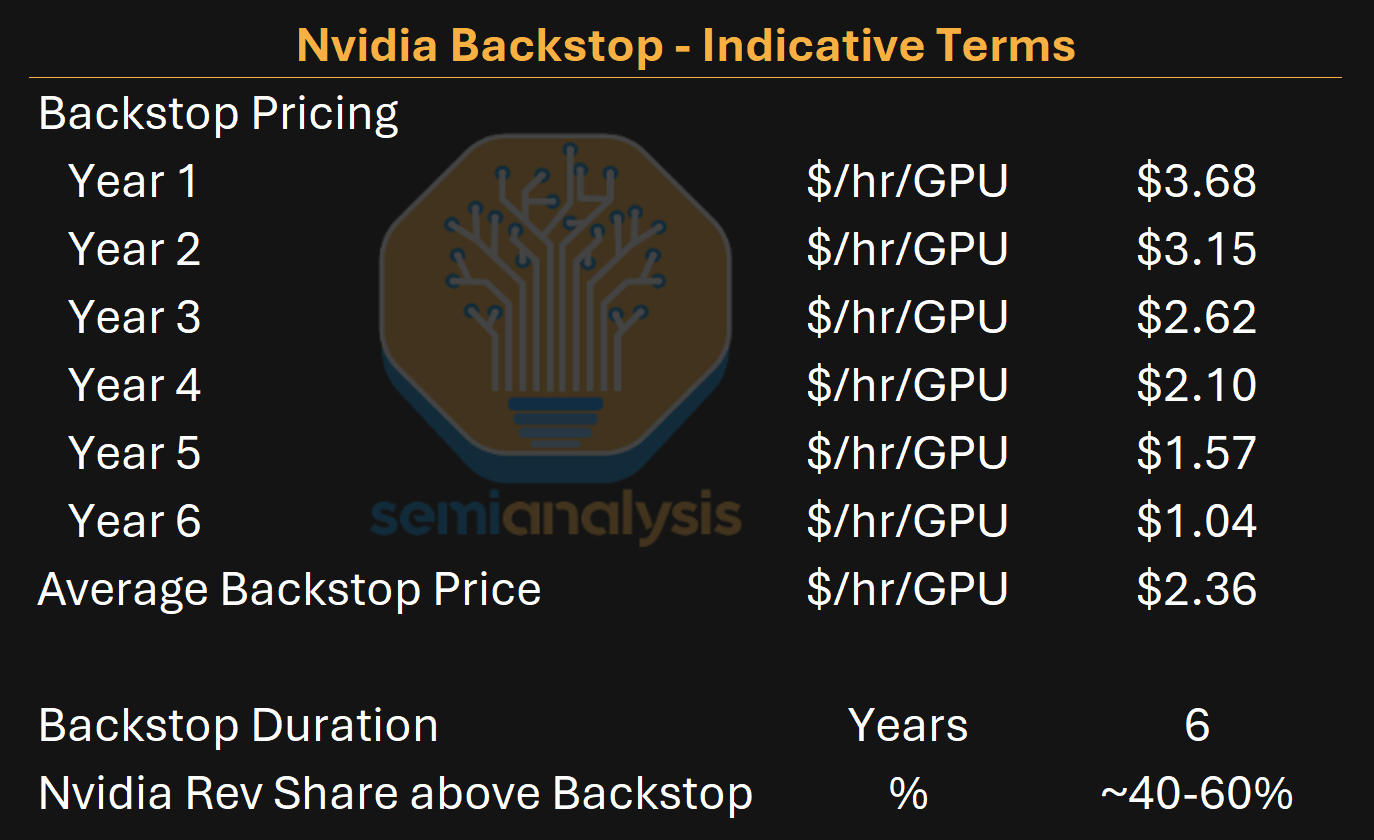

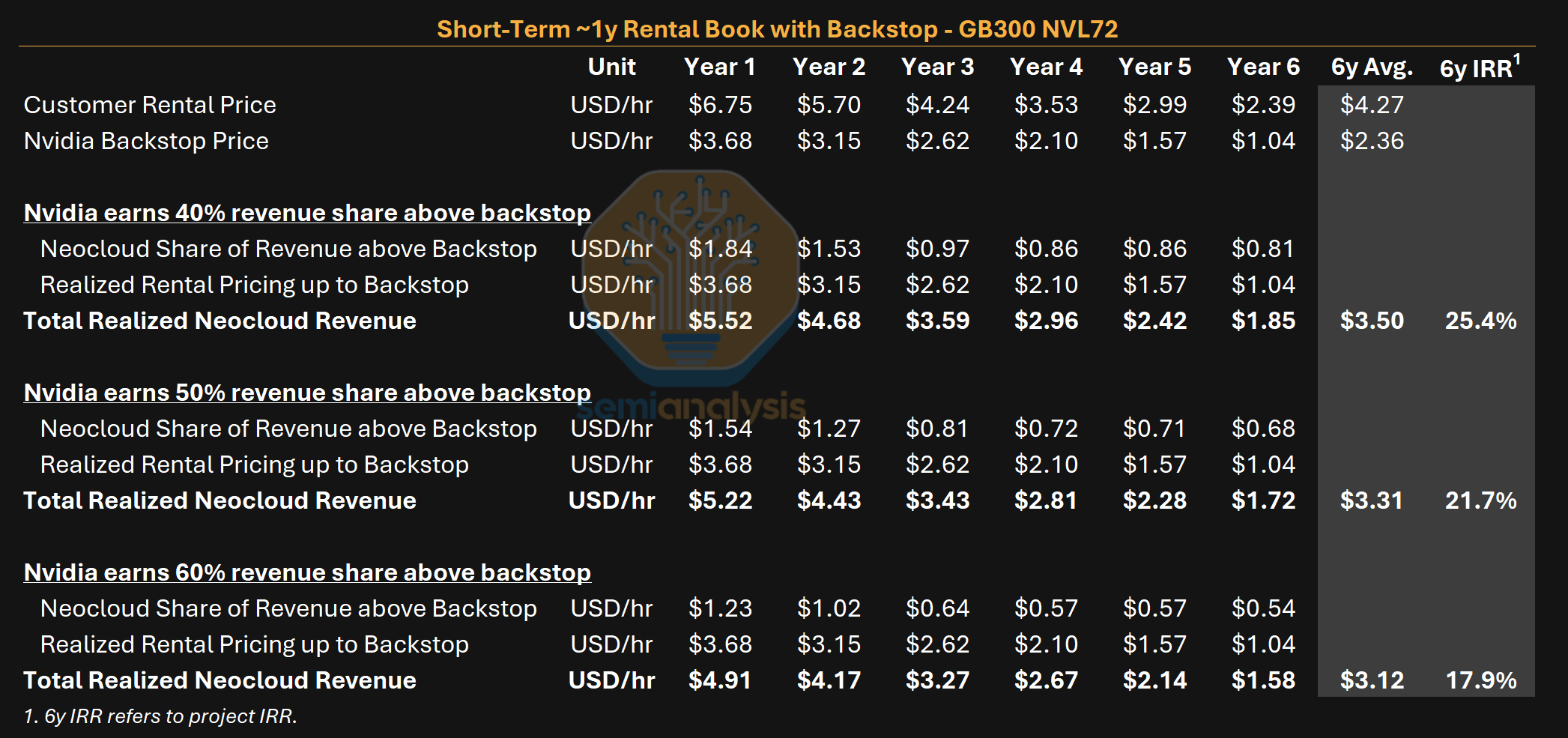

Nvidia’s backstop program is typically six years in length, and during these six years, Nvidia stands ready to purchase compute at pre-agreed price levels that vary over the time period. Each Neocloud is expected to negotiate the backstop terms individually, and we can expect that different Neoclouds may end up with different revenue share and backstop schedules. The below table is an illustrative example to explain the basic terms of the program – we present a backstop pricing curve that we believe to be on the lower end of the backstop range – in this case at an average of $2.36 over the six-year period, but we expect that most Neoclouds will negotiate higher backstops.

Let’s start by exploring Neocloud economics under the backstop program by considering a few different scenarios. In the first scenario, the Neocloud focuses on a customer base that rents at a 1-year or lower tenor, so we model the 1-year rental price for a GB300 starting at $6.75/hr for the first year before decaying over time as the overall market cost of compute declines. As with any business that is operating a “curve trade” – that is investing long and renting out on shorter tenors – we should expect that in theory the average realized rental price over the project lifetime should be slightly higher than the current 6y fixed price of ~$4.00. This is to compensate the Neocloud for taking on future price risk.

In any given year, the Neocloud will earn 100% of the rental price up to the backstop amount, but in respect of the amount which the rental price exceeds the backstop, the Neocloud will share a portion of this revenue with Nvidia.

In the table below, we show workings for this scenario. Let’s walk through an example of how to calculate the Neocloud’s revenue share. In the case where Nvidia earns 40% revenue share, we see that in year 1, the Neocloud will charge its customers $6.75/hr on average. Of this, the Neocloud earns the full amount up to Nvidia’s year 1 backstop of $3.68/hr, but for the difference between $6.75/hr charged to customers and the $3.68/hr backstop amounting to $3.07/hr, Nvidia will earn $1.23/hr and the Neocloud will earn $1.84/hr. In total, the Neocloud will realize $5.52/hr for the first year, which of course is lower than the $6.75/hr that they would have earned without the backstop. Over the six years of this scenario, the Nvidia take rate works out to be about 18% on average, but without the backstop, there would be no cluster!

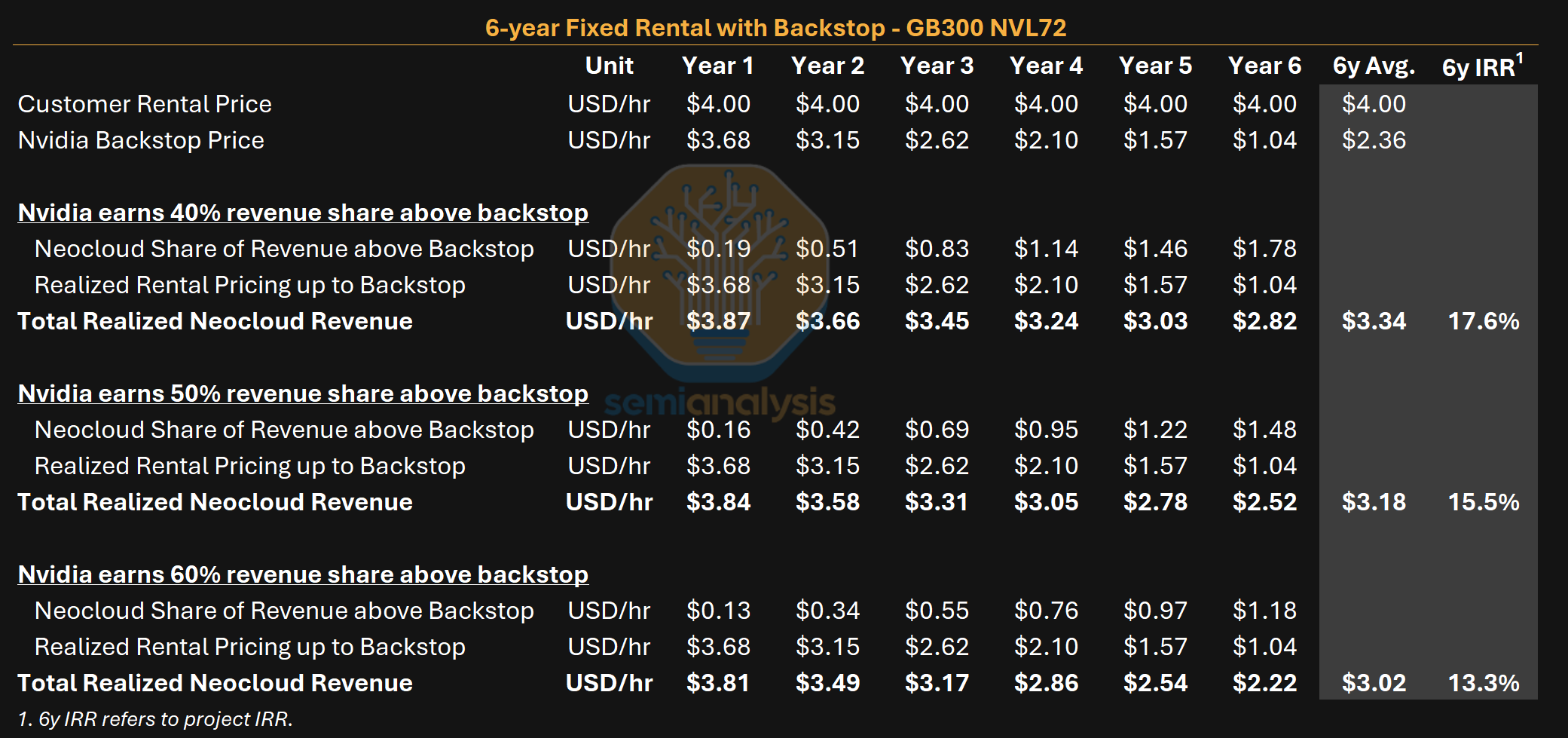

Our second scenario analysis illustrates how the backstop math would work with a 6-year fixed price offtake. This scenario is admittedly an oxymoron – if you can get a 6-year fixed price offtake, then you of course do not need an Nvidia backstop and would thus would certainly not want to pay the revenue share out to Nvidia. Turning around and renting out compute on a 6-year contract would also be against the spirit of Nvidia’s backstop program as this deal would do nothing to further the objective of supplying compute for shorter tenors to a variety of different buyers, especially emerging workloads.

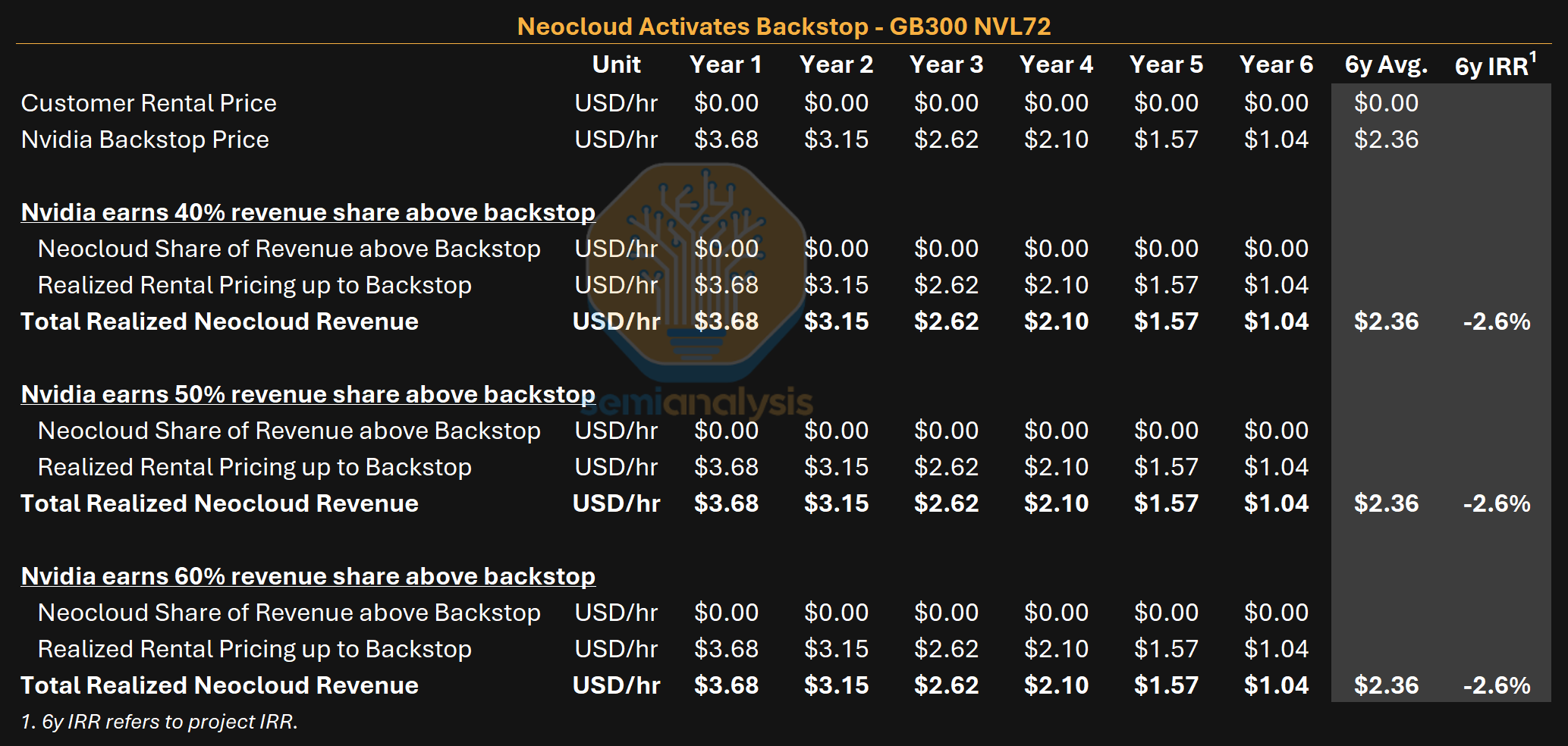

It is important to highlight that while Nvidia does have meaningful internal compute needs, neither Nvidia or the Neoclouds have any intention of using the backstop, and thus it is not surprising that the backstop levels would result in a typical Neocloud earning a zero or slightly negative project IRR.

In the table below, we illustrate the economics of renting to Nvidia under the backstop. This scenario would only materialize if the Neocloud is unable to find sufficient third-party customers at market-clearing rental and must activate the backstop.

That said, this scenario is exactly why the structure is financeable. Though the IRRs earned under this scenario will turn out to be near zero or even slightly negative, the Neocloud will at least still be able to cover debt payments, making lenders comfortable with this structure. Loan underwriting for clusters with an Nvidia backstop will evaluate debt service coverage ratios in the scenario in which the backstop is triggered to determine how much funding can be provided.

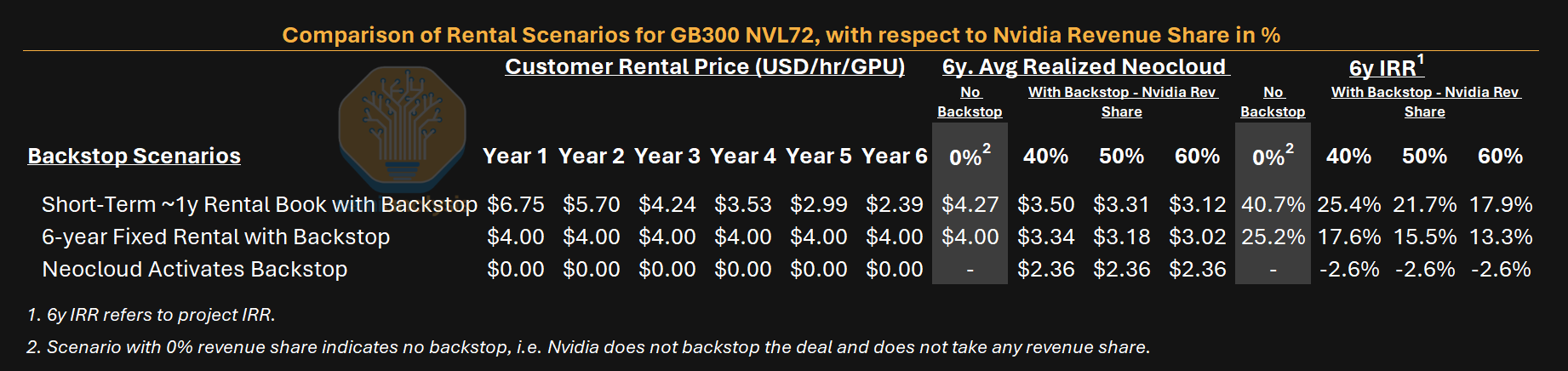

The table below summarizes the return profiles under the various scenarios discussed above as well as displaying the economics of a Neocloud renting at the same prices but without any backstop.

We see that the short-term 1y rental book scenario clearly offers the best IRR among the backstopped scenarios at 25.4%, and these IRRs could realize even higher if the rental market turns out to be strong enough such that 1y and shorter rental rates decay by less than we modeled in the curve below. As expected, the IRRs are higher without a backstop – reaching as high as 40.7% when renting for 1y tenors with no backstop. But if Neoclouds activate the backstop and rent to Nvidia at those prices, they can expect to earn zero or negative IRRs.

How to Price a GPU Loan

Many lenders are already being sounded out on the Nvidia backstop structure. They use the typical hyperscale backstopped compute deals as a starting point for their credit assessment but instead substitute Nvidia’s credit rating.

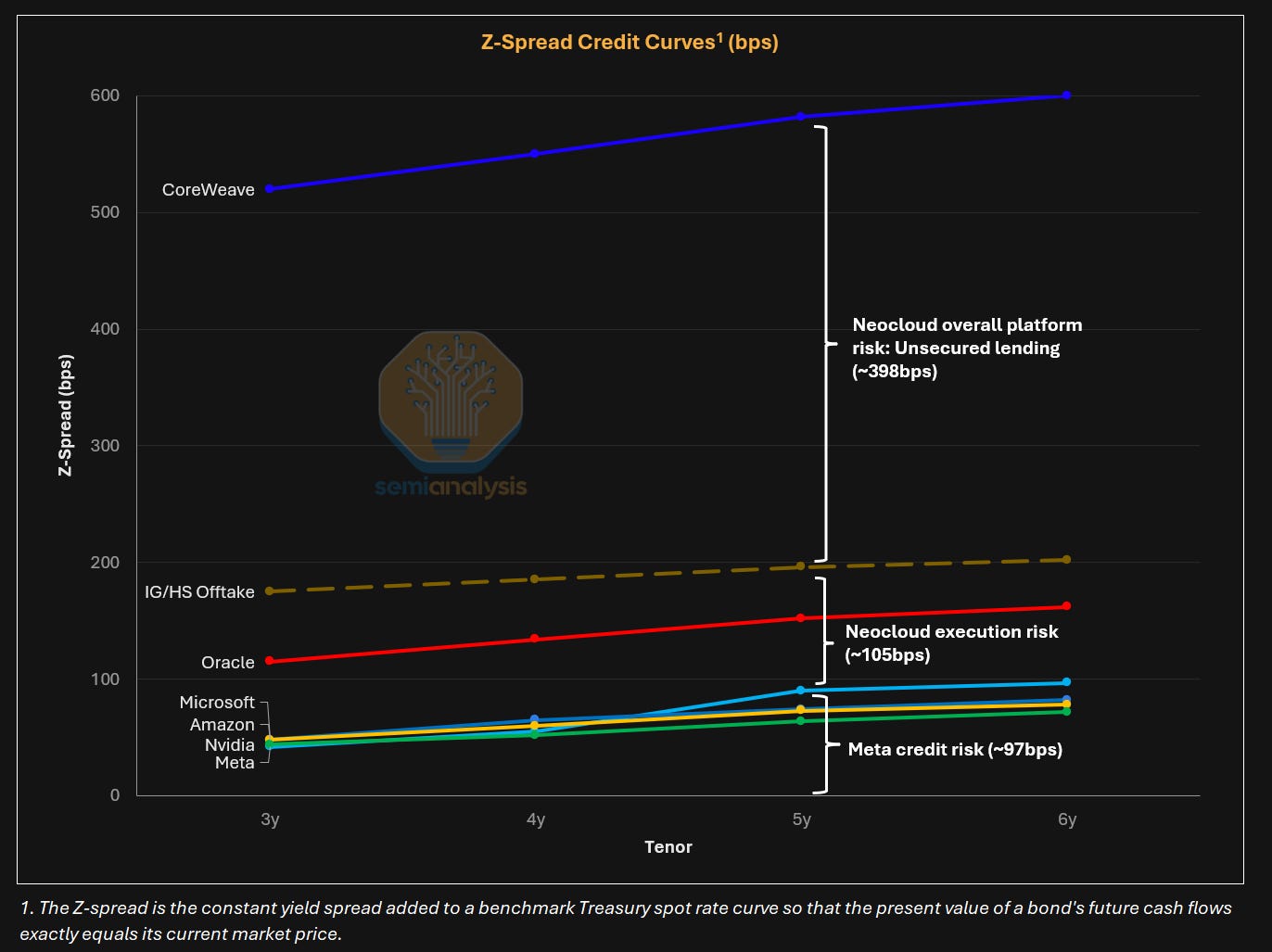

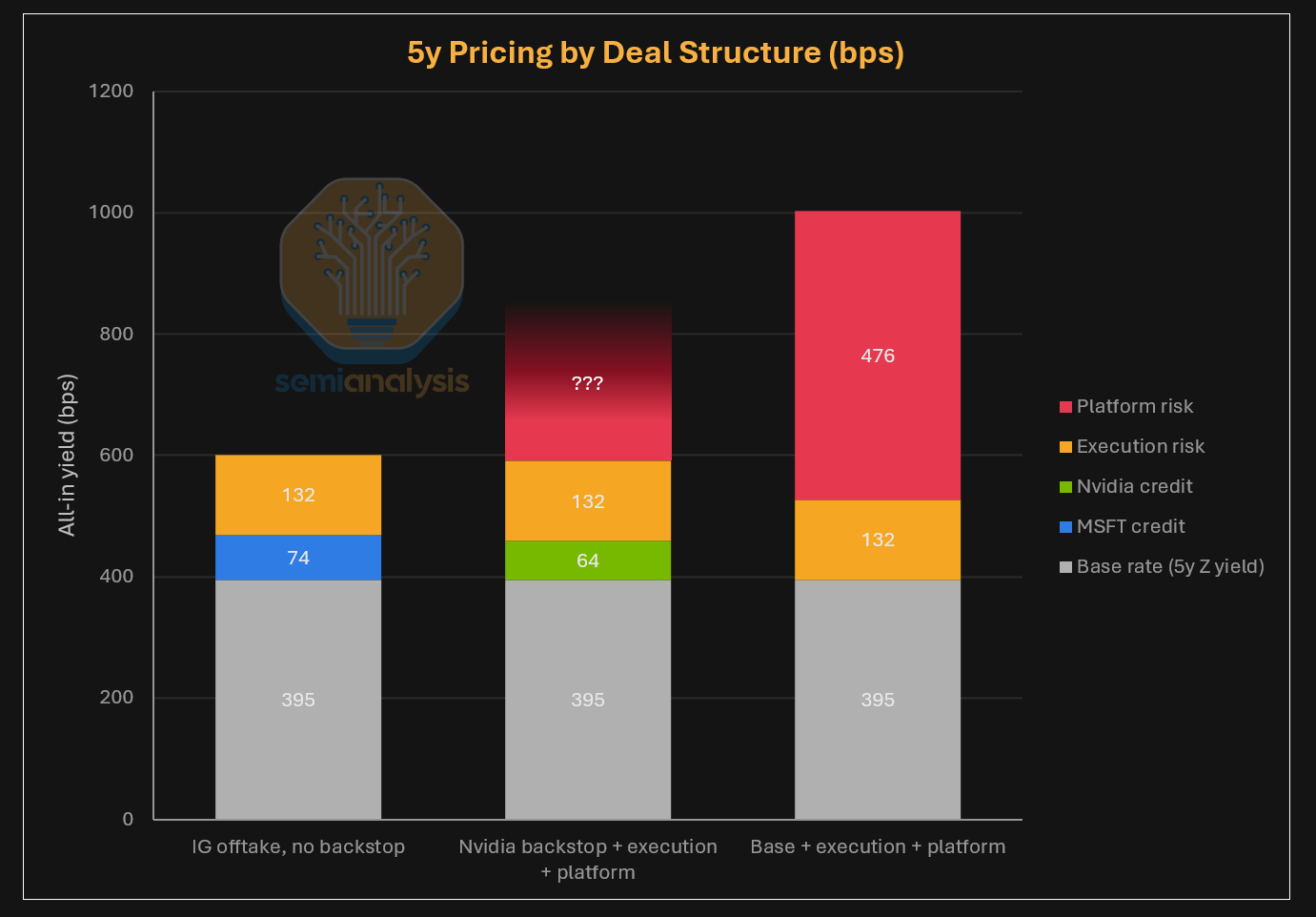

Let’s briefly review how the GPU financing market works before we explain how this market is evolving to cater to the Nvidia backstop. Pricing for Neocloud financing with a long-term offtake is heavily driven by credit spreads for the hyperscaler or other company that is providing the offtake as opposed to following the Neocloud’s credit spreads. Instead – the Neocloud’s execution risk is what drives the spread above the underlying hyperscaler’s credit spread.

Readers may notice the huge gap between CoreWeave 5y unsecured bonds at ~10% and the 5.9% that CoreWeave paid for the fixed-rate tranche of their DDTL 4.0 $8.5B delayed-draw term loan, which was backstopped by Meta. This 5.9% yield works out to about 90 basis points wider than Meta’s 5y bond yield of ~5.0%. This can be interpreted as the market pricing CoreWeave’s execution risk with respect to that particular project at 90bps.

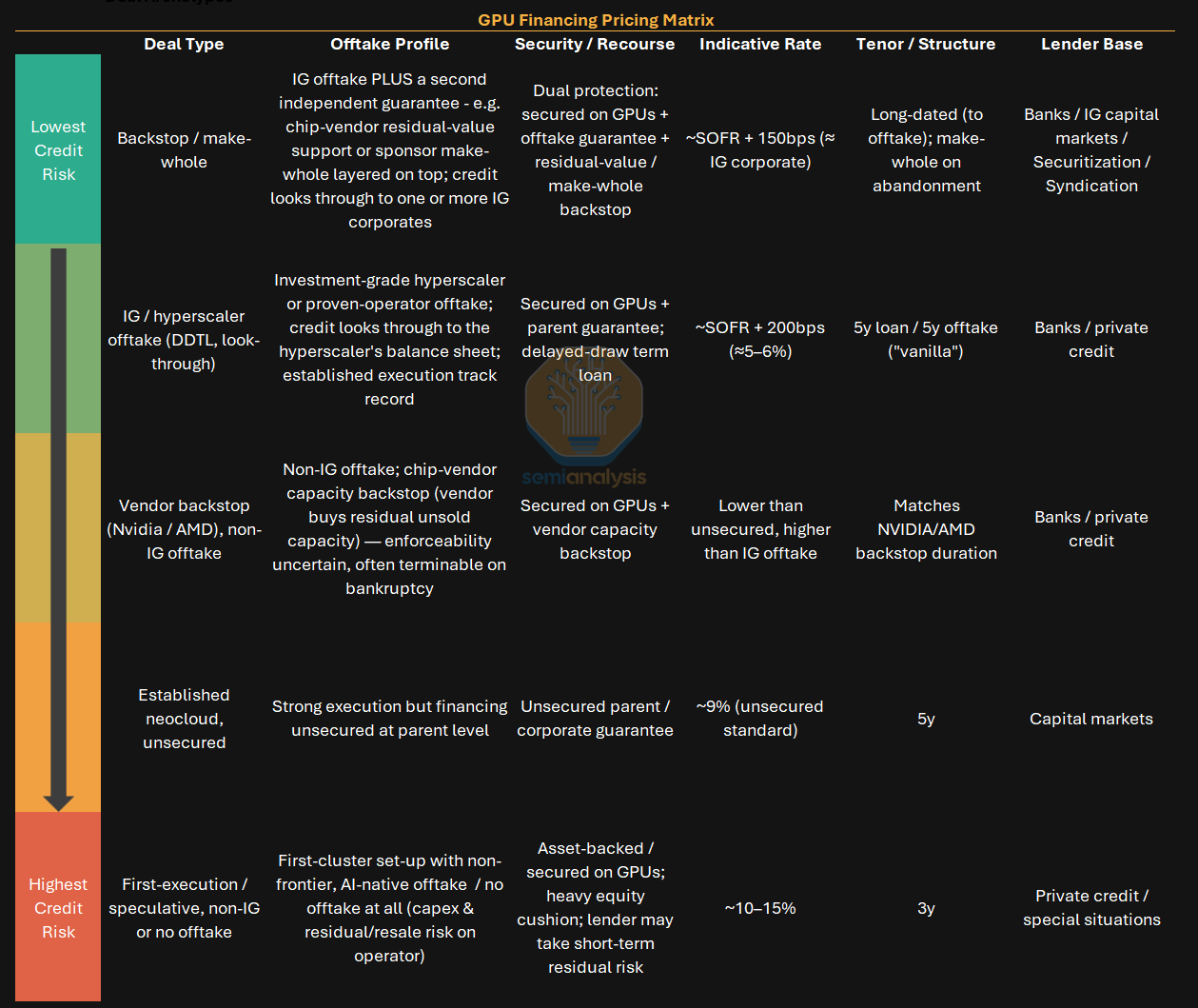

We breakdown the main type of financing we see today in the table below from lowest credit risk to highest credit risk.

A natural question to ask is why has financing not evolved outside the four walls of 5-year IG offtake take-or-pay contracts? Neocloud financing has been challenging because it involves financing a complicated and novel stack of infrastructure and IT equipment where end demand for tokens is still new, not well understood by lenders, and lacks a long history from which to draw insights on risk management from. For lenders, it is much easier to focus on the hyperscaler offtake or backstop as there is no need to dive deep into tokenomics or rapidly evolving AI models and delve into the minutia of which scale-up network topologies perform best on the all to all collective – at the end of the day, it is hyperscaler risk.

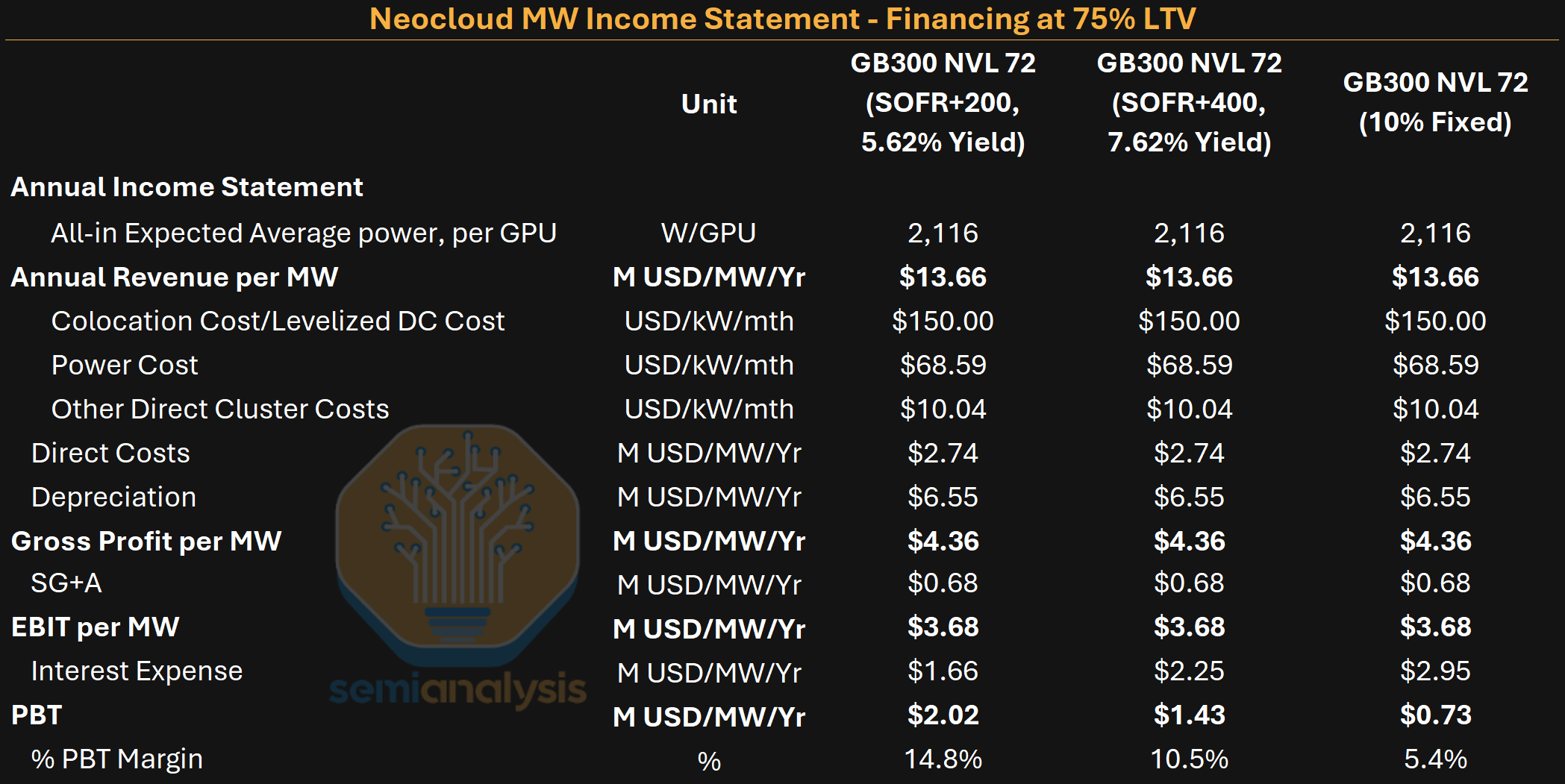

Neoclouds have also had a strong incentive to stick with this recipe. To fund a cluster that they intend to rent on shorter terms with a broad book of customers, a Neocloud would have to fall back on unsecured funding. For a top Neocloud, this would mean paying an additional 4% interest, which would significantly impact the economics of the deal given the 70-80% loan to value ratios used to finance GPUs. In our modelling, we show that increasing funding from an all-in cost of 5.62% to an all-in cost of 10% drops PBT margins from 14.8% down to only 5.4%. Unsecured lending to a top Neocloud would probably be around 10%, but expect even more expensive unsecured financing for smaller Neoclouds with a shorter track record.

Lastly, let’s discuss how banks will size lending to Neoclouds.

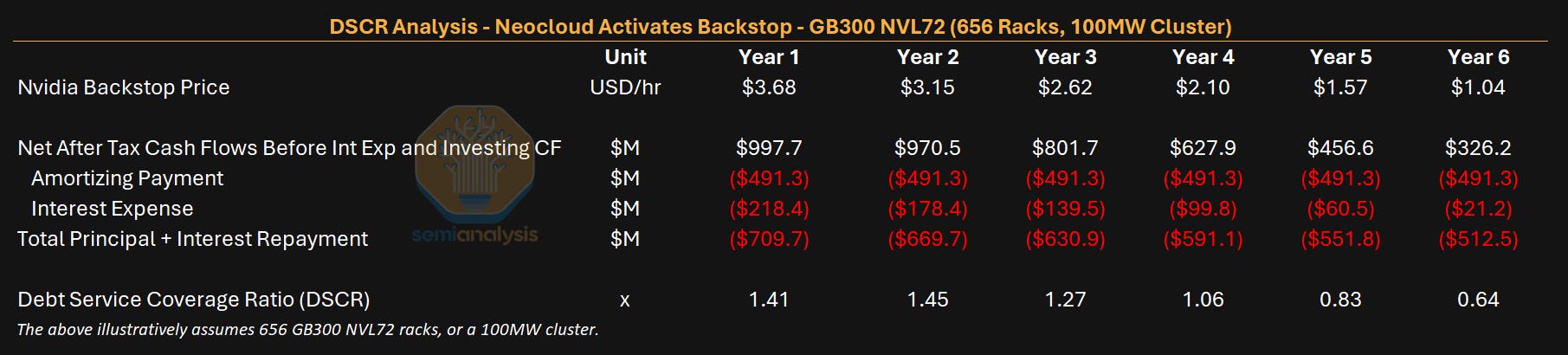

The most important debt ratio that lenders look at is the debt service coverage ratio (DSCR). DSCR is calculated as the ratio of the project’s cash generation divided by total debt interest and principal payments in each period, and it is a measure of how well covered the debt payments are by the cash flow of the business.

When it comes to the Nvidia backstop, banks look at the DSCR ratios assuming revenue earned under the scenario where the backstop is activated. They are looking for a DSCR of at least 1.3x, particularly for the first few years of GPU financing agreement and size their loans to ensure that this bar is met. This typically corresponds to a 70-80% loan to value (LTV) ratio.

Great Expectations – How the GPU Financing Market will Come of Age

GPU financing will have to rapidly evolve if it is to meet the staggering capital needs we outlined earlier in this article, and financing Nvidia backstopped clusters is the vanguard of this huge shift. Lenders in the past were not comfortable financing projects with price risk and have wanted a long-term offtake from a strong credit, a residual value cushion, a parent guarantee, a vendor backstop or some other floor under the asset. However, lenders are now starting to look deeper into Neoclouds’ business models, with our assistance and due diligence consulting services. Even though they have the Nvidia backstop in their back pocket, the highest quality lenders are now utilizing SemiAnalysis to scrutinize Neoclouds’ operational quality, go to market plan, customer book and pricing strategy.

This is a healthy development – and the Nvidia backstop provides the support that lenders need to get up the curve and prepare for the era when they will finance Neoclouds as a standalone platform basis without any external backstops or guarantee, just like they would understand any other business they lend to that invest in the long term yet are exposed to shorter-term price risk – be it petrochemical companies, memory chip manufacturers and the like.

We think that initial lending will be at a wider spread than the current 5y backstopped hyperscale deals which come in at around SOFR + 225bps (roughly equivalent to a Z-spread of 195bps, or about 5.9% total yield) but at a tighter spread than CoreWeave’s 5-year unsecured corporate bond which has a yield of ~10% (roughly equivalent to Z-spread of 600bps).

Tools that GPU Lenders Will Need

Lenders will also need tools to price and manage risk in the new GPU lending world order. They will need a good GPU rental price index, a way to forecast GPU rental prices into the future and a model for estimating and tracking GPU residual value over time. They will need some way to differentiate among operator quality and a framework for understanding the differences in operator capability. They will also need to be able to model end demand, and how token demand maps into GPU demand.

Luckily – at SemiAnalysis, we have already launched products that address many of these needs!

Our GPU Rental Pricing Index tracks bilateral contract prices across the entire term structure, from on-demand to 5-year deals, across all major GPU SKUs, giving lenders and investors a transparent, transaction-validated benchmark where none previously existed. The H100 1y index is freely available for public use!

Meanwhile, our AI TCO Model has been forecasting GPU rental prices since 2023 and provides a complete three statement financial model complete with return metrics like IRR, return on invested capital, debt service coverage ratio and more. In our consulting practice, where we have provided technical and consulting due diligence to clients that have provided tens of billions in capital to Neoclouds, we have used the AI TCO model as a tool to validate many of their commercial assumptions and help underwrite the investment cases. The AI TCO Model also includes a framework for calculating GPU residual values and much more.

ClusterMAX is the only Neocloud rating system in the industry. Our ClusterMAX rating system evaluates GPU cloud providers across 10 criteria including reliability, networking, and pricing, giving capital providers a standardized quality framework to assess counterparty and collateral risk. We do significant custom diligence as ClusterMAX cannot be used for commercial purposes without our authorization.

Our tokenomics practice tracks end token demand and consumption closely across hyperscalers and AI labs with a focus on SKU and model level ARRs for all key labs, model performance, token pricing, and more.

Lastly, our InferenceX benchmarking product continually measures and tracks real-world GPU inference throughput and token efficiency across inference systems, models and software configurations, enabling lenders and operators to quantify the productive output, and therefore the revenue-generating capacity, of a cluster they are financing. It is an important resource for mapping token demand into GPU demand.

Current and Future Backstop Activity

Nvidia’s backstop program is only getting started, and we see announcements coming faster every quarter. Many Neoclouds are already deep in negotiations with Nvidia, and there are still others that are considering engaging with the backstop program. Let’s briefly discuss the deals that have been announced to date – all of which are in the Asia Pacific region so far.

The first is SharonAI’s 72MW AI factory in Australia. Announced in June 2026, the deal has SharonAI scaling up to as many as 40,000 GB300s under a six-year backstop. Sharon disclosed a total backstop value of $4.88B, which works out to an implied floor of about $2.33/hr/GPU on average over the six year period. Sharon AI’s footprint is now set to grow to 132MW with 102MW contracted, and the company guides to reaching more than 55,000 Nvidia GPUs in total (inclusive of the 40,000 GB300s backstopped) by mid-2027.

Firmus’s 360MW AI Cluster in Batam, Indonesia is the next major project announced with an Nvidia backstop. It will likely be housed in a DayOne facility in Kabil Industrial Tech Park (KITP). Announced just recently on June 29th, 2026, this project shows the scale at which Nvidia is rolling out the backstop program. Firmus’ first clusters were based in Singapore and focused on H100s deployed using immersion cooling. The next key cluster launched was the 18,000 GB300 cluster in Melbourne, Australia housed in a 42MW self-built datacenter. This project was financed using a $10B USD facility led by Blackstone (Tactical Opportunities, Credit and Insurance) and supported by Coatue.

The Nvidia backstop allows Firmus to grow their business by an order of magnitude. As per Nvidia’s key objectives that we outlined above, the focus of this cluster will be to open up compute to a variety of AI Natives, Enterprises and Inference Providers, with many different rental tenors to be offered. Firmus announced that they expect $25B to $30B of customer revenue over the six years. We expect a portion of the revenue above the backstop level will be shared with Nvidia as per the structure we outlined earlier today.

Beyond this – Firmus also announced a 600MW firm-energy deal with Gunvor that will also underwrite 1.2GW of new renewables development and 1.5GWh of storage in South Australia by 2032. Firmus will still need to identify a datacenter provider or build their own datacenters before they can deploy GPUs.

We have seen many other neoclouds having backstops, but many are not public yet.

Nvidia is not the only merchant GPU vendor to utilize backstops. AMD has already been providing backstops starting last year. We wrote in our AMD article from June 2025 that AMD offered AWS, OCI, Digital Ocean, Vultr, Tensorwave, Crusoe and other Neoclouds a backstop deal, whereby in exchange for customers’ willingness to buy more AMD GPUs, AMD will stand ready to rent back a significant chunk of this capacity in the form of long-term contracts for internal AMD software development purposes if the Neocloud isn’t able to full sell their capacity.

There are many more deals in the works and we believe that many of the clusters announced to be built in partnership with Nvidia will later be confirmed to be built atop an Nvidia backstop. In the next section, we will explore how this revenue backstop will affect Nvidia’s balance sheet and income statement.