Intel Should Raise Capital

Intel's woes are behind them. The heavy spending is ahead of them. Why an equity issuance in a hot equity market could make Intel so much better sooner.

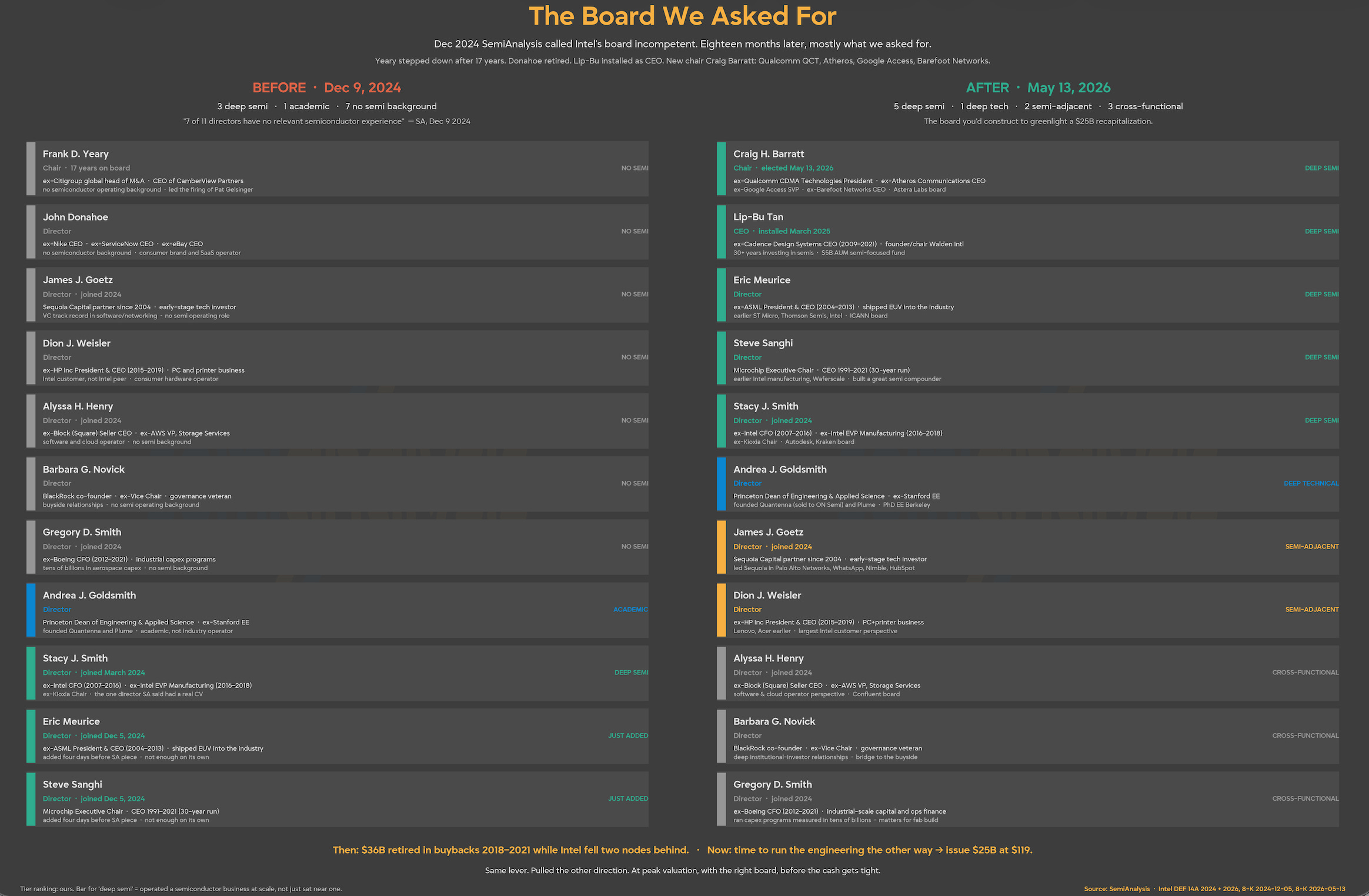

We have written a lot about Intel. It’s a firm near and dear to our heart, and is the birth of the semiconductor industry. To say we love Intel and their role in the world is an understatement. We also have been very vocally right during their initial product mishaps, as well as supportive and excited for the turnaround. The thing we have believed the most is that Intel’s board is one of the biggest parties to blame for Intel’s death, and we recently got what we want.

Intel on the Brink of Death | Culture Rot, Product Focus Flawed, Foundry Must Survive

Intel’s board is incompetent and its horrible decisions over the decades are going to push it towards death. The decision to fire Pat Gelsinger, put in charge a CFO + career sales and marketing leader, and cut spending on fabs in favor of a renewed focus on x86 is an example of the incompetence that will end Intel.

Franky Yeary just stepped down from the board after 17 years, and now the new board is filled with people who actually understand the industry, and not financial engineering. The new chair is ex-Qualcomm, Lip Bu Tan is the CEO, and Steve Sanghi of Microchip, Stacey Smith, Eric Meurice of ASML are all there. The board actually understands technology. But while Intel’s turnaround has partially begun, there is a lot more on this long road to a completely revitalized Intel. Today we think that Intel should make another large strategic bet with their fresh board, and it’s instead of buying back shares, it’s time to issue enough shares to fix Intel’s finances for good.

Lip Bu Tan has taken Intel back from the brink, and has raised ~20 billion dollars from the government stake, Softbank, Altera and Nvidia’s strategic investments. They should not stop partially, and capitalize on share prices. They were large net buyers of shares during the bad years, it’s time to issue equity into strength, and if they do it right, it will make Intel’s turnaround that much more successful.

Dilution Here Rewards The Investors Who Already Bet

Look at where that capital came in. The U.S. government took up to 433 million shares at $20.47, a 9.9% stake at signing, with 149 million still in escrow at the end of Q1. SoftBank paid $23.00, Nvidia paid $23.28. Every one of those holders is already above water.

So the instinct that a raise punishes the people who just showed up runs the wrong way. Issuing stock at today’s price, well above those entry marks, lifts book value per share and hands the government, SoftBank and Nvidia a gain. That 10% sovereign anchor is also the reason a large offering clears cheaply in the first place. Intel is one of the very few companies on earth that can sell size into a hot tape with the U.S. government holding the floor, and that is leverage worth using while it exists.

Intel Needs Capital for Execution

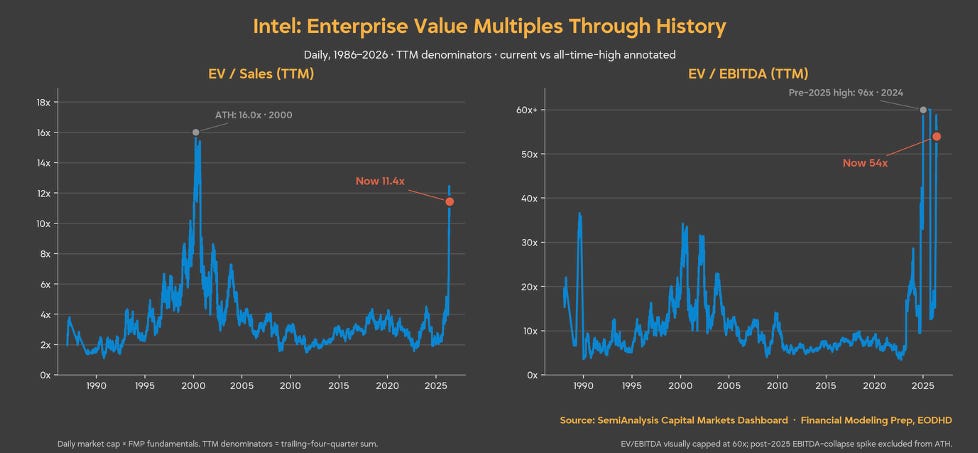

Intel has pretty much never traded this expensive on a trailing twelve month basis since the 2000 bubble. While we believe there is a bright future, one of the most critical things it will take is capital, and the share price is not discounting real execution risk.

What’s more, even in the best of cases from the new renewed demand from Agentic CPU, Intel cannot pay for the best of upsides even. We think it’s time for Intel to do a reverse buyback, and issue equity during this equity demand window.

Equity Is Now The Cheapest Money Intel Can Get

The objection will be that Intel has other ways to fund a fab. It tried all of them, and just told us they don’t work. Apollo put $11.2B into 49% of the Fab 34 joint venture. Brookfield structured the Arizona build. Silver Lake took 51% of Altera at an $8.75B enterprise value, netting Intel about $4.3B. Intel sold its NAND business to SK hynix in stages and sold additional Mobileye shares. Smart Capital was the whole identity.

Then, on March 31, 2026, Intel agreed to buy Apollo’s 49% of Fab 34 back, closing April 8 for $14.2B, roughly $7.7B of cash and a $6.5B bridge loan. Management called the unwind accretive, and they were right, which is the whole point. If buying a fab stake back is accretive, then selling fab economics to a partner was expensive money all along. A SCIP hands a sponsor a permanent cut of your best asset in exchange for capital that costs more than it looks, and Intel has now shown with its own checkbook that it would rather own the fab and carry the debt.

So cross the alternatives off. More SCIPs are the option management just spent $14.2B reversing. More debt stacks on top of the $45.0B already on the balance sheet, roughly $51.5B once the Apollo bridge is in. The largest asset monetizations have already been substantially harvested. Intel sold control of Altera and has monetized part of Mobileye, while retaining approximately 48% and 78%, respectively. Further sales remain possible, but these are no longer untouched sources of capital at the scale previously available. Against this valuation, equity remains Intel’s cheapest scalable source of capital.

The foundry business is just beginning with their large Terafab announcement as well as overflow demand from the great N3 shortage. To truly capitalize on this special moment, Intel must be the great supplier of the rest of the industry hungry for leading edge wafers. And that huge bet requires capital well in excess of their ability to fund from operations today.

Just a 4-5% dilution would raise ~$25 billion dollars and easily allow for the most bullish supply capacity story to come true during this critical time.

Agentic CPU Demand Ain’t Enough to Pay for Terafab

SpaceX and Tesla as well as Terafab is the large customer commit that solves the 14A capacity issue. And the initial target of 100k WSPM scaling to 1 million (going to be hard) is going to be extremely rough in terms of capital. This needed to happen, as Lip Bu Tan has publicly told the market he would shut Foundry down if there were no customers. And now that a customer has come, its time to build.

Beyond the Terafab partners, the order book is filling in. Nvidia’s DGX Rubin NVL8 lists dual Intel Xeon 6 host CPUs. Google signed a multiyear deal covering Xeon and custom IPUs. SambaNova came in on inference. The wafer volumes behind these wins are not all disclosed, but capital markets fund a visible book far more cheaply than they fund a turnaround story, and Intel finally has one to point at. An equity raise sold against signed demand prices very differently from one sold against a promise.

Intel has been working it’s absolute hardest to defer capex on lower than expected demand for CPU, but it’s time to bet the farm again ala Gelsinger style. This is the critical moment for silicon sovereignty, and its time to press.

The full multi-phase project for Intel is going to cost up to $119 billion dollars, and while SpaceX is putting up the initial capital, Intel has to contribute meaningfully. Even a marginal amount of capital matching means that this is 10s of billions of dollars that were not in the capex decision matrix just a month ago.

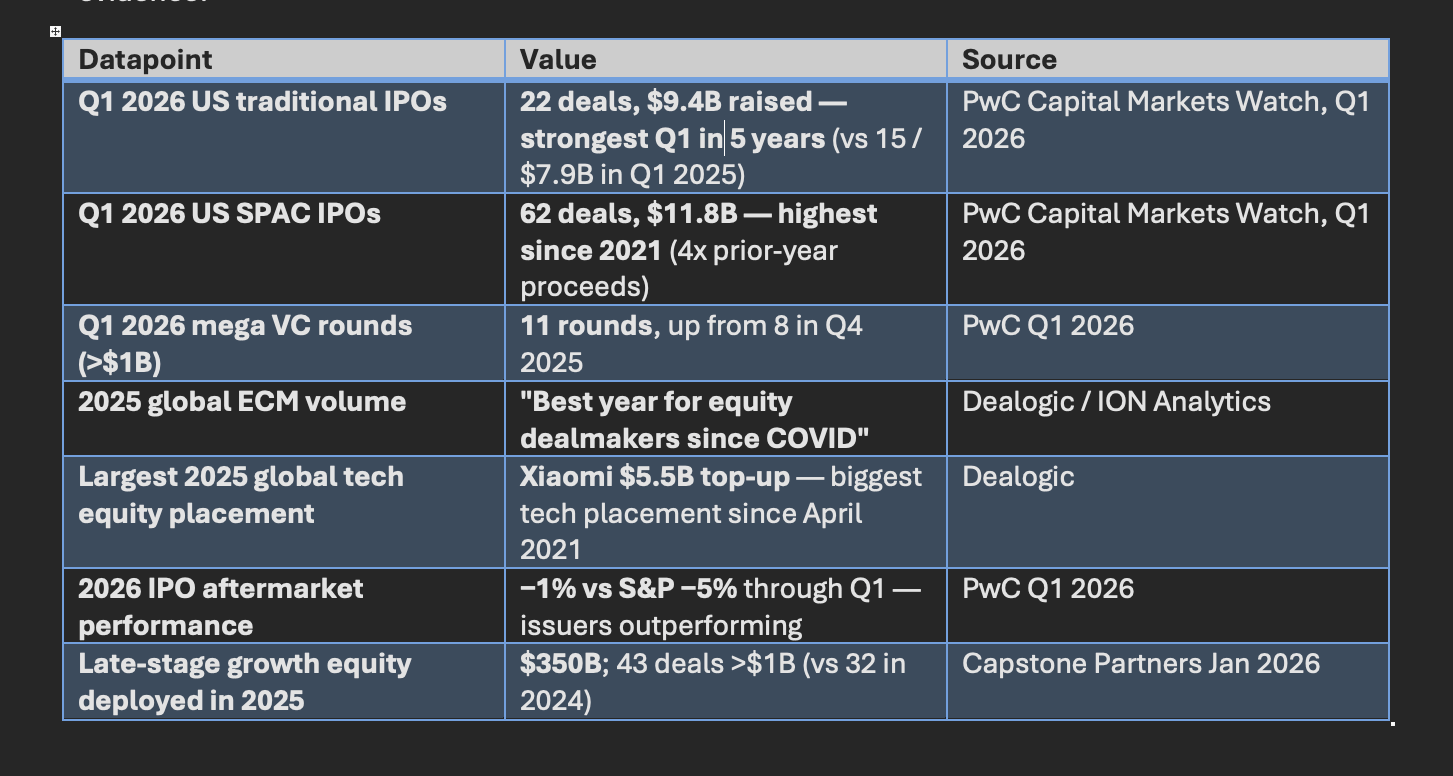

It’s time to undo a decade of financial engineering and issue equity now. Because while the ramp is exciting, it’s going to cost a lot. The equity issuance window is the biggest it’s been in a moment, and if Cerebras can raise 5.55 billion, Intel can raise 25. The point only gets stronger, since Intel’s roughly $498B market cap easily supports a far larger follow-on. The window as we see it seems to be wide open, here’s some stats from other issuance recently.